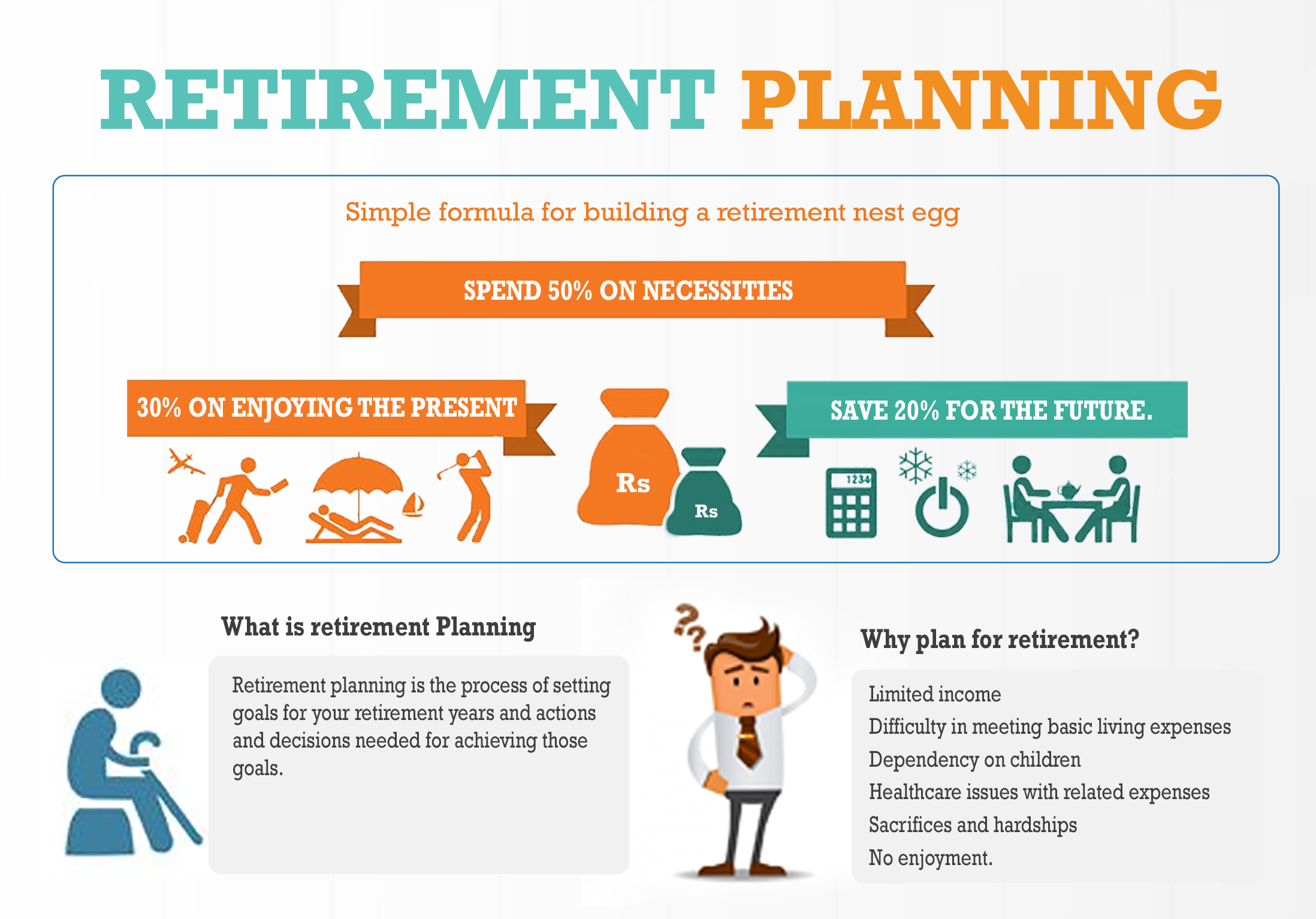

Managing debt is one of the most important steps toward financial freedom. Whether you owe money on credit cards, personal loans, or mortgages, being in debt can feel overwhelming. However, with the right strategy, discipline, and commitment, you can reduce your debt faster and more efficiently than you might think. This article explains proven methods for cutting down debt, organizing your finances, and staying on track until you are debt-free.

1. Understanding the True Cost of Debt

Before taking steps to reduce debt, it is essential to understand how debt affects your financial situation. Debt is not only about the amount you owe but also the interest you pay over time.

1.1 How interest increases your debt burden

Interest is the cost of borrowing money, and high interest rates can cause balances to grow quickly if not managed properly. For example, if you have a credit card with a 20 percent annual interest rate and only make minimum payments, it could take years to pay off even a moderate balance.

1.2 Why understanding your debt matters

Knowing exactly how much you owe, who you owe it to, and what interest rates apply allows you to make informed decisions. Without this clarity, it is impossible to create an effective repayment plan.

Start by listing:

- All debts (credit cards, loans, mortgages, personal lines of credit)

- The total amount owed on each

- Interest rates and minimum payments

- Payment due dates

This gives you a complete picture of your financial obligations and helps prioritize which debts to pay first.

2. Create a Realistic Debt Reduction Plan

A clear, structured plan makes debt repayment achievable. Without a plan, payments may be random and progress will be slow.

2.1 Choose a repayment strategy

There are two popular approaches to debt repayment:

- The Debt Avalanche Method

- Focus on paying off the debt with the highest interest rate first while making minimum payments on others.

- Once the highest-rate debt is paid, move to the next one.

- This method saves the most money on interest over time.

- The Debt Snowball Method

- Focus on paying off the smallest balance first to gain quick wins.

- As each debt is eliminated, apply the freed-up money to the next smallest debt.

- This method builds motivation and psychological momentum.

Both methods work; choose the one that best matches your financial and emotional needs.

2.2 Set a monthly budget

A detailed budget helps you allocate funds to essential expenses while directing extra income toward debt repayment. Track all income and expenses to identify where you can cut costs. Small sacrifices, such as reducing dining out or entertainment expenses, can accelerate debt reduction.

2.3 Use a repayment schedule

Create a timeline with clear milestones. Seeing your progress over time motivates you to stay consistent.

3. Reduce Interest Costs and Fees

Interest and late fees can keep you trapped in debt longer. Minimizing these costs can speed up repayment significantly.

3.1 Negotiate with lenders

Contact creditors and request a lower interest rate or a payment plan. Many lenders prefer to work with borrowers rather than risk default. A reduction of just a few percentage points can make a big difference over time.

3.2 Consolidate your debts

Debt consolidation combines multiple debts into a single loan with a lower interest rate. This simplifies repayment and can lower monthly payments. Examples include:

- Personal consolidation loans from banks or credit unions

- Balance transfer credit cards with promotional zero percent interest periods

- Home equity loans (if you own property and understand the risks)

Before consolidating, ensure that fees or extended loan terms do not offset the benefits of lower interest.

3.3 Avoid new high-interest borrowing

Once you start repaying debt, avoid taking on new loans or credit card balances. Continued borrowing can undo your progress and increase financial stress.

4. Increase Your Income to Accelerate Debt Repayment

Reducing expenses is important, but increasing income can significantly speed up debt elimination.

4.1 Explore extra income opportunities

- Freelance work, part-time jobs, or consulting in your field

- Selling unused items online or through local markets

- Offering tutoring, ridesharing, or delivery services

Every additional dollar you earn can be used to reduce your principal balance faster.

4.2 Direct windfalls toward debt

Tax refunds, bonuses, or gifts should go straight to debt repayment rather than discretionary spending. One-time lump-sum payments can dramatically shorten your repayment timeline.

4.3 Automate extra payments

If your income allows, set up automatic additional payments each month. Automating ensures consistency and prevents temptation to spend that money elsewhere.

5. Manage Spending and Build Better Habits

Financial discipline is key to staying debt-free once progress begins.

5.1 Track your expenses daily

Use a spreadsheet or a budgeting app to monitor where your money goes. Awareness is the first step toward control.

5.2 Differentiate needs from wants

Before making any purchase, ask yourself if it is necessary or simply desired. Prioritize needs until your debt is under control.

5.3 Build an emergency fund

Unexpected expenses often push people back into debt. Save at least three months of living expenses in a separate account. Even a small emergency fund provides a financial cushion that prevents reliance on credit cards.

5.4 Avoid emotional spending

Recognize triggers that cause you to spend impulsively. Emotional spending often leads to unnecessary debt and regret. Replace this habit with healthier stress-relief alternatives like exercise or hobbies.

6. Seek Professional Guidance When Necessary

If your debt feels unmanageable despite your best efforts, consider professional help.

6.1 Credit counseling agencies

Reputable credit counseling agencies can review your financial situation, negotiate with creditors, and design manageable repayment plans. Look for agencies accredited by national financial organizations and check reviews before enrolling.

6.2 Debt management programs

These programs consolidate payments and may reduce interest rates through agreements with lenders. While they can be helpful, ensure you understand all fees and potential effects on your credit score.

6.3 Bankruptcy as a last resort

Bankruptcy should be considered only after exploring all other options. It can provide relief for severe debt situations but has long-term consequences for credit and future borrowing ability. Consult a financial advisor or attorney before making this decision.

7. Conclusion

Reducing debt quickly and efficiently requires structure, persistence, and discipline. The process begins with understanding the total amount owed and creating a realistic repayment plan using either the avalanche or snowball method. Cutting unnecessary expenses, negotiating lower interest rates, consolidating debts, and increasing income all accelerate progress. Equally important is building healthy financial habits such as consistent budgeting, avoiding impulsive spending, and maintaining an emergency fund. With patience and consistent effort, becoming debt-free is not only possible but sustainable. Debt freedom offers more than financial relief, it provides peace of mind and the freedom to focus on long-term financial goals such as saving, investing, and building wealth.

FAQs

What is the fastest way to pay off debt?

The fastest way to pay off debt is to use the debt avalanche method, focusing on high-interest debts first while maintaining minimum payments on others. Increasing income and cutting expenses can also accelerate the process.

Should I consolidate all my debts into one loan?

Debt consolidation can simplify payments and reduce interest, but it works best when the new loan has lower rates and no excessive fees. Always compare total repayment costs before deciding.

Can I pay off debt without harming my credit score?

Yes. Making on-time payments, avoiding new credit inquiries, and lowering your credit utilization can actually improve your credit score as you pay down debt.

How much should I pay toward debt each month?

Aim to pay more than the minimum required. Even an additional 10 to 20 percent each month can save years of repayment and hundreds in interest.

Is it possible to reduce debt while saving money?

Yes. You can build a small emergency fund while paying down debt. Once you have a safety net, direct any extra funds toward repayment. This balance prevents setbacks from unexpected expenses.